Happy April! In case you missed it, I continued the April Fools’ Day tradition around here with a bit of fun-poking around the idea of “mindset” and FI foods. Once the cat was out of the bag about the joke, I turned it into a game with a fun little prize: an Amazon gift card for whomever can name the most sources for the fun food references in the post! There are still a few days left and no one has yet been able to name all 33, so that prize could be yours!

In the meantime, let’s jump on into March’s numbers:

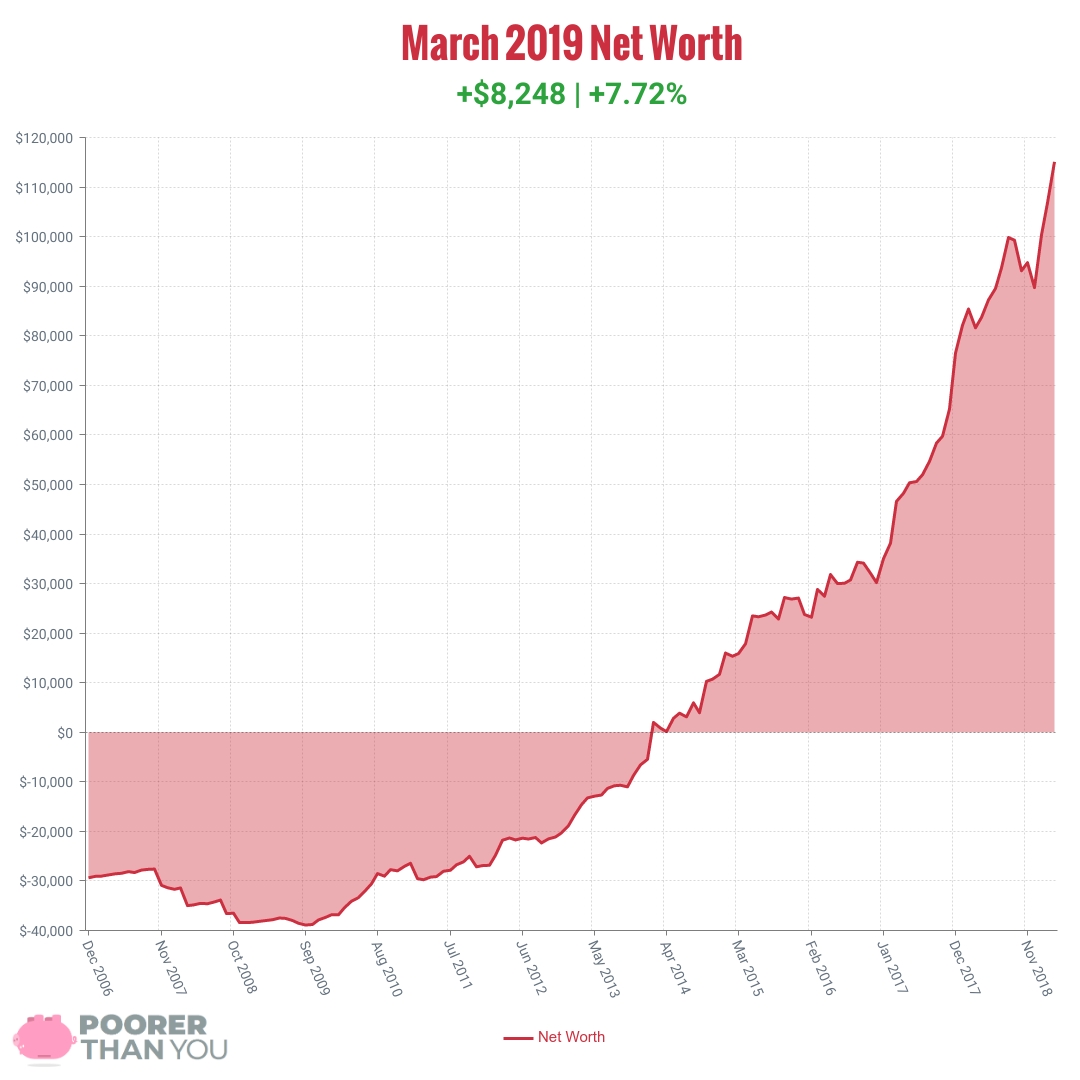

Change: +$8,248 or +7.72%

March Net Worth TOTAL: $115,063

Another month of doing okay!

Another month of doing okay!

I’m kidding. EIGHT FREAKING THOUSAND DOLLARS WHAT?!? Even though that’s not my “best month ever,” that’s amazing!

The explanation, though, is really pretty simple.

Cash: +$870

Most months I’ve been hoarding cash for bank account opening bonuses and for my upcoming dental work (oh joy). But this month, not so much! Instead, we dumped cash into our 2018 Traditional IRAs (Individual Retirement Accounts). This was planned for, so it wasn’t a hit, but it does mean that cash didn’t grow much this month, despite getting a big ol’ fat tax refund.

Okay, understandably, some folks really may wonder why I chose to get a big tax refund this year, rather than keep my withholding low and invest throughout the year.

Well, the simple answer is: a lot of things changed from last year’s taxes, and we had absolutely no idea what this year’s taxes were going to look like. I didn’t know that my freelance client was going to stop giving me work, so I was withholding assuming that I’d get about $15,000 in work from them again in 2018, but instead, I got $0. Which is fine, but it means I over-withheld. By a lot.

We also didn’t qualify for Obamacare (ACA) subsidies in 2018 because, well, we were no longer on an ACA plan! So we didn’t know how that was going to shake up our taxes, and better safe than sorry to over-withhold.

So we got a big tax refund and we shoved it all into Traditional IRAs, which further grew our tax refund. It’s a fun virtuous circle that never ends! Until you hit the $5,500 per person contribution limit, that is. ($6,000 per person in 2019.)

Retirement: +$6,848

Right, so, I put $5,500 into the Traditional IRA. And I did my normal HSA contributions from my paycheck, as always. The remaining $700 or so was stock market growth, and that’s all she wrote!

Car: +$63

My car value is up again this month. Still basically irrelevant, still don’t know why it would be going up several months in a row… maybe 2004 Camrys are super hot right now? I know teens these days are wearing 90s mom jeans, so maybe it’s related. Seems like if you’re wearing mom jeans as a norm-core fashion statement, you probably need a silver Camry to complete the look.

Other Assets: -$15

My Lending Club account is nearly depleted! Gone soon, I imagine. Alas, poor Lending Club… it never lived up to what I wanted it to be.

Student Loan: -$150

Last month there was no change because the short month meant my end-of-February payment didn’t show up. Well, this month, we get the two-fer! February and March payments now reflected, so it’s double down. How exciting!

Credit Card: -$108

0% interest credit card and I have the cash to pay it off so I just pay the minimums for now… if you’ve been following along a while, you know the drill here!

One little fun update: Bank of America actually sent me an email this month to let me know the exact date that the promo rate is ending, and give me 90 days of warning. That’s nice, because I don’t like relying on my own calculation of “I signed up this date and it was a 15-month promo, therefore…” Seems too likely that I’d get hit with some sort of “gotcha.” But to have the end date in writing from the bank itself? PERFECT!

Other Debts: -$225

Car insurance payment month! Which means the “debt” that I calculate as growing every six months to pay it is now paid off. And it starts again!

Milestone Progress

Debt Freedom: No extra payments this month (again), so May 2024 is still the calculated date. Still more literal teeth to pull (and to pay for) and then I can think about switching us to debt-payoff mode again.

$200,000 in Retirement Accounts: Currently at $113,218 with $86,782 left to go! The “goal” is to hit it 5 years after hitting $100k in retirement, which is 53 months from now. That will take growth/contributions of about $1,637/month. That seems very reasonable, once we get past all this “paying for dental work” stuff, anyway!

Not super exciting in the explanation this month, but that’s how I like it! Boring, with big numbers.

I run these numbers by hand in a spreadsheet, and you could do the same, or you can check out Personal Capital for some automagical tracking. You and I each get a $20 Amazon gift card if you sign up through me and then link it up to at least one valid investment account.

Either way, add it up and let me know how you’re doing in the comments, below!

Time Travel

- Previous month’s net worth update (February 2019)

- One year ago (March 2018)

- Five years ago (March-December 2014) (the dark time, when I wasn’t allowed to write in this blog!)

- Ten years ago (March 2009)

- Go back to the very beginning (December 2006)

Photo credit: Steppinstars

Big woots on maxing out the IRA!

I’m surprised BofA sent you that warning for the promo ending, I would have expected them to keep quiet about that to make money off you.

Our March was boring except for terrible spending for vet care and life insurance. Booo.

No one was more surprised to see that email from BofA than me! 😀 That certainly didn’t happen with either of my previous 0% interest balance transfers. (And one of those was BofA, too! But like, 11 years ago.)

Sorry about the pet care expenses. That’s one small “benefit” of my husband’s allergies (skipping those costs), but of course, I know how bad it can get – when I was a teenager, my dog stole an entire 18 pack of hot dogs and a pack a buns from a cookout I was hosting… and that was a $5,000 bill. I was old enough at the time to understand the full extent of what that meant. (My parents paid it, somehow…)

That’s a really fantastic acceleration in wealth building. Keep it up!

Thanks for sharing but what is really the point of these type of posts? Can you write more articles about how to help people build their wealth instead of just showing off your own?

I am glad you are building your net worth, but it really doesn’t help anybody else.

Hi Lizzy, thanks for coming by. This is my personal blog that I’ve been keeping for over 12 years. I try to find time to write more than the net worth posts, but some years (like right now when I have a young toddler), it’s very hard. Many people have found the fact that I manage to keep up at least the net worth posts helpful, so I continue to do them. They are certainly helpful for me, and they are what allow me to write posts like this one, that show more of the big picture. You may find it more helpful to find some of my net worth posts from back when my situation was more like yours, if you cannot relate to my life as it is now. Or, maybe, this just isn’t the blog for you.

As a stand-alone post, I can see how someone would view a post like this as not very useful. However, over time, I think they’re amazingly beneficial to folks other than the original author.

You get a peek into their real-time issues related to their finances. You can see how that changes over time when you keep up with them. You see how they respond to new milestones, challenges, market swings, etc.

I love net worth posts, and it’s why I post them as well. I’m always excited for the end of the month when I get to see how everyone fared against their own goals throughout the year. This blog is always one of my first stops at the top of each month.

Thank you, Debt Ascent, that’s really amazing to hear! Do you think I could do anything better with these posts in terms of showing that they’re not meant to be stand-alone bits? I try to link to my other net worth posts within each one whenever relevant, and I did the big “look back” connecting 10 years of them together, and of course I have the “time travel” section at the end of each one now so that people can jump around to see how it compares. But since the original idea (12 years ago, when I started) was to show the whole journey from negative net worth and poverty upward… can you think of anything that’s missing to connect each new post the whole?

Can I think of anything that’s missing? Not at all. If anything, I have a lot to learn from you about how to tie these reports together into a cohesive story.

Your about section on the right hand side of this page reads: “Stephonee… has been sharing her personal finances, observations, and real talk about money on Poorer Than You for 10 years – a third of her life.”

This post is saying and doing exactly what you warned them you were going to. 🙂 In my view, someone who sees these posts as braggadocios or “look at me” is missing the point and hasn’t dug too far into your archives.

The best part about net worth posts is that you can click on them if you want to and find them interesting and/or helpful

– or –

you can also do what I call the “do not click” and go on about your day.

Based on the other comments, it seems the balance is definitely skewed positive/helpful. Sorry for the mini-rant. Looking forward to your April update.

Hi – I don’t agree. There are hundreds of articles on wealth building, all pretty much the same. Articles on peoples actual wealth is rare and I love reading other peoples stories. It brings it all back to reality.

If you don’t like it, don’t click it!

Thank you Jim! I think the stories are the most important part – I learned from other people’s stories over the years, so I try to share mine, as it happens! I’m really proud that I now have 12 years of real-time stories on here because of that.

Yes! It’s also rare that people share their wealth-building from the beginning of their journey … and not just once they’ve hit FIRE or whatnot. I find these posts immensely motivating.

Sorry, but I agree. If all Steph is going to do is post her financial progress, that’s nice and all, but not very helpful when there are no useful tips.

It’s just a “look at me” and that’s it.

The truly great blogs are ones that help readers instead of just focusing on oneself.

I look forward to reading more helpful posts!

I have to say, I’m a bit shocked by these reactions. In 12 years of publishing these net worth updates, I’ve never had feedback like this. And with all of these other comments giving the opposite feedback, I’m not quite sure how to respond. The purpose of the net worth posts has been, the entire time, to show my personal journey from a negative net worth, no job, college dropout, to what I hoped to become someday (which I’m still figuring out as I go, but I’m certainly in a place now that I couldn’t have imagined back at the start!).

There are 528 posts published on this blog. Less than 1/5th of those are net worth posts. If you cannot find the “useful tips” in the more than 400 other posts on this blog, or within the net worth posts, I don’t believe you’re going to find them here in anything new that I write. This blog may just not be the one for you, if that’s the case. And that’s alright! I’m just not sure what it is that you do want from me that led you to comment saying you don’t see the point in what I post in my personal blog.

Way to go on the net worth increase!

I’m still waiting for my tax refund (long story, but it’s going to be at least another couple of months, I think), but that’ll be a big boost to my overall net worth. And like yours it’ll mainly go into a retirement account. Like you, my refund came because I had no idea what to expect on my taxes. I divorced, so I had to figure my single taxes for the year, which apparently were way off. So… refund.

I think cash going up by $870 is pretty woot-worthy, personally. But then again I’m currently splitting my excess cash among my mortgage, retirement accounts, emergency fund and savings account (and only really feel like I’m “saving” the savings account amount) so my progress feels a lot more incremental than yours.

Good luck on the dental work!

I’m really excited now about the $870 cash increase… because I have the orthodontist appointment scheduled for next week! *It’s happening!!!* May’s net worth post is probably going to be a real down, heh, but all these ones where things went up will cushion the blow!

I love seeing the actual numbers. You’re doing great and you’re honest about anything that isn’t “optimized.” These posts make me think, “oh, I remember how it felt to hit that milestone, how exciting!” and also, “dang, I can’t wait to hit that number, good for her!”

Thank you Meagan! I really love when we as a community can celebrate each other’s milestones. I know not everyone is comfortable sharing, but I know there are some people who feel like they get to celebrate along with me because I share, and that’s great, too!

I love seeing your net worth posts. You have posted some great articles on your personal experience with savings and debt, so it is great to see how your efforts, routines, and strategies have led to progress. I hope you keep posting updates to inspire others.

Thank you Pai! I definitely plan to keep posting these updates, and I hope I can also find time to do other types of posts as well. 🙂

I love real world numbers to relate to. And pair that with the “Time Travel” section you can really see how sticking to a plan over the long run can make a sizable difference. When you’re in the slog of paying off debt/ saving for retirement on a smaller salary it seems that you’re going no where. This illustrates actual situations that are relate-able.

Thank you for sharing when not everyone does.

Thank YOU Shauna! I’m glad the Time Travel section is helpful, since that’s a recent addition that I thought of. I’m still working on going back and adding it to older posts, as well, so it’s good to have the feedback on it and know that it’s something worth spending time on, when I get a chance. 🙂

While I don’t do net-worth posts myself, I think they can be a great service. People who are in debt will see real-world examples of how debt can be managed and ultimately beaten.

And as others have noted, readers can watch your progress and realize, “I’m making progress as well — maybe not as fast as I’d like, but change IS occurring.”

Not all bloggers are financially independent and/or rich. All readers aren’t, either. There’s a story for every reader and a reader for every story.

Wise words from one of my long-time blogging idols—thank you so much, Donna!

Love it! Congratulations! $8000 is fantastic in a month! Keep it up! We don’t share our info but I’m really amazed and impressed how compounding does work even though it has worked for us for years it still gives me goosebumps when it goes up.

When the market does go down like I experienced in 2008/2009 we kept on investing even with low returns we knew it would go up. Keep on going!

Congratulations!

Thank you, Holly! I know another market downturn is inevitable, and there will be more bumps along the way, but I do hope I can keep contributing no matter what curveballs come my way. 🙂